Key Takeaways

- The CPG market is growing, but supply chain complexity is rising with it.

- Efficiency alone is no longer enough in a volatile, value-driven market.

- Fragmented systems and SKU complexity are limiting agility.

- AI, regionalization, and automation are reshaping CPG supply chains.

- True advantage comes from aligning technology, data, and operations.

For decades, supply chains in the consumer goods industry were designed for a relatively stable world. Global sourcing reduced input costs and increased bargaining power with suppliers. Expanding portfolios secured shelf space, and forecasts relied heavily on historical demand patterns. In that environment, efficiency became the dominant measure of success.

That stability has gradually given way to uncertainty.

From Stability to Volatility

The shift is unfolding in an industry of massive scale. The global consumer packaged goods market was valued at roughly USD 3.45 trillion in 2025 and is projected to exceed USD 4.2 trillion by 2030. As the market grows, so does the complexity of managing sourcing, production, and distribution across regions.

Today, trade policy volatility, geopolitical tension, and regionalization are reshaping sourcing economics. Nearly half of global consumers identify as value seekers, adjusting purchases based on price perception and economic conditions. Retailers are expanding private-label portfolios while tightening control over consumer data, and artificial intelligence is transforming how planning and operational decisions are made.

Yet many organizations still operate supply chains built for predictability rather than volatility. Industry maturity remains modest, and the profitability gap between leaders and laggards continues to widen.

To understand the scale of change underway, here are some key statistics shaping the global consumer goods and CPG landscape.

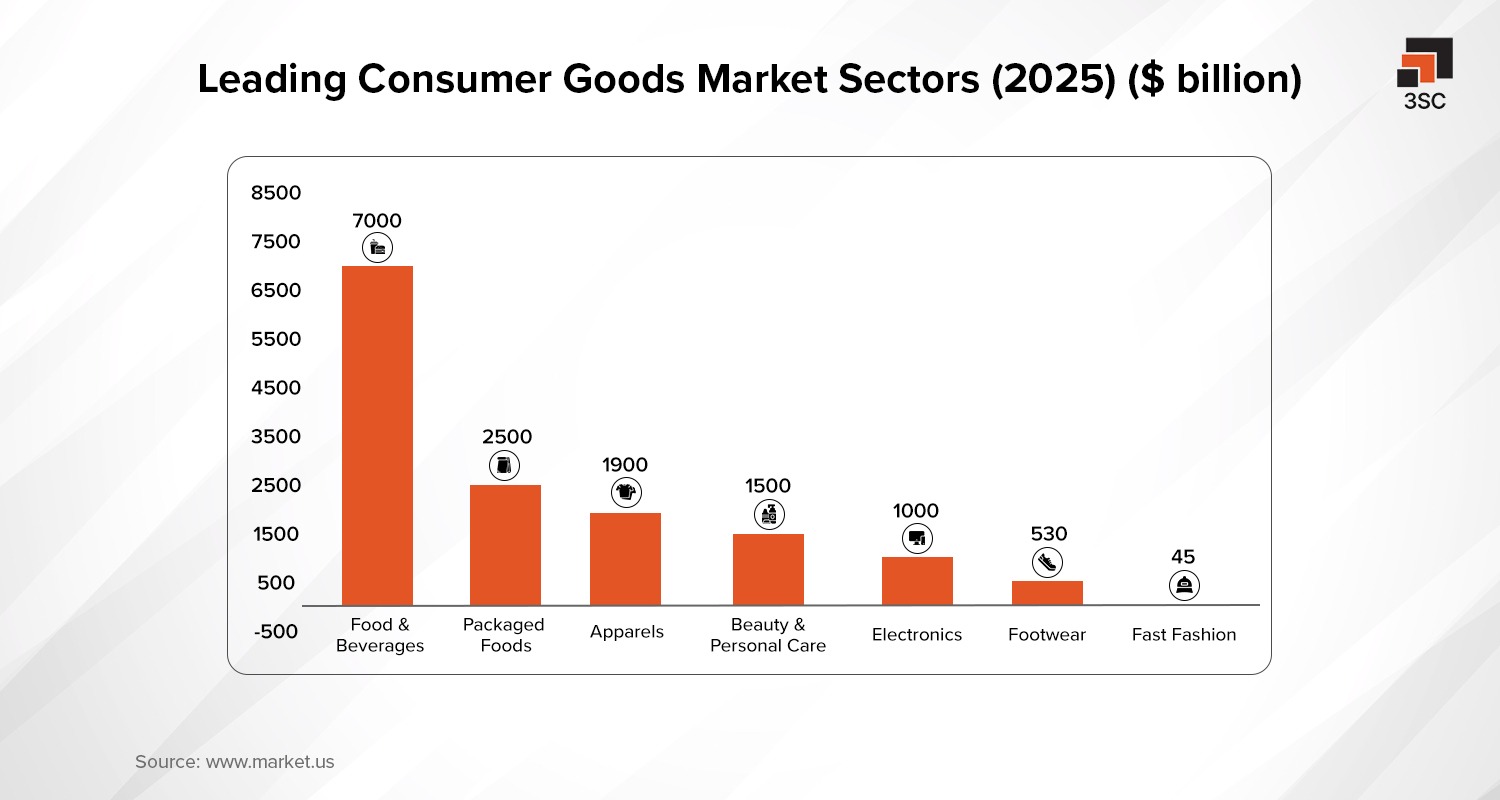

Topmost Important Consumer Goods Industry Statistics

As per Market.Us Report (2024-25)-

- The global consumer goods market is valued at USD 12.5 trillion in 2024 and is projected to reach USD 18.5 trillion by 2031, growing at a 4.8% CAGR.

- The consumer-packaged goods (CPG) market stood at USD 5,467.5 billion in 2024 and is forecasted to grow to USD 7,799.4 billion by 2033.

- 73% of global consumers are willing to pay more for eco-friendly brands, highlighting sustainability as a key purchase driver.

- 57% of consumers research products before purchasing, while impulse buying has dropped to 18% in 2024.

- Some of the world’s most influential CPG companies include: Nestlé, Procter & Gamble, Unilever, PepsiCo, The Coca-Cola Company, Mondelez International, L'Oréal, Danone, Colgate-Palmolive, Johnson & Johnson

Overall, the consumer goods industry continues to scale steadily, powered by digital acceleration, sustainability-driven demand, and strong growth in emerging markets.

To move forward, we must first understand how the CPG supply chain functions end to end, then examine where it is under strain, and finally explore the trends and solutions shaping 2026 and beyond.

Understanding the End-to-End Consumer Goods Supply Chain Process

The consumer goods industry supply chain is an interconnected system. Every stage influences cost, agility, service levels, and resilience downstream. From product design to final delivery, every step plays a defined role in moving goods efficiently across the value chain.

Let’s walk through the full journey of an average CPG brand.

1. Portfolio & Product Planning: Where Complexity is Born

Supply chain design starts with portfolio and product decisions.

Each SKU influences forecasting requirements, production scheduling, warehousing needs, and transportation planning. Product design choices such as packaging formats, ingredient selection, and promotional strategies directly shape downstream supply chain activities.

Portfolio planning defines how products will be positioned, produced, and distributed across markets. These decisions establish the foundation for sourcing strategies and operational planning.

2. Sourcing & Supplier Networks: The Resilience Backbone

Sourcing determines how raw materials, components, and packaging inputs are secured.

Organizations develop supplier networks based on geographic reach, production requirements, and strategic priorities. Sourcing strategies often include supplier diversification, multi-supplier models, and integration of ESG criteria into procurement decisions.

Supplier relationships are increasingly structured around collaboration, performance tracking, and long-term alignment. Once inputs are secured, materials move into manufacturing for conversion into finished goods.

3. Manufacturing & Production Planning: Converting Strategy into Output

Manufacturing transforms raw materials into finished products. This stage includes capacity planning, production scheduling, labour allocation, and quality control. Production plans are aligned with demand forecasts to ensure output meets market requirements.

Many organizations use advanced planning systems and scenario modelling to coordinate production activities and maintain alignment between supply and demand.

4. Demand Forecasting & Inventory Strategy: Navigating Uncertainty

Demand forecasting estimates future product demand using multiple data inputs. These inputs include retail sell-through data, promotional plans, e-commerce activity, and regional demand signals. Forecasts guide production volumes, procurement planning, and inventory positioning.

Inventory strategy determines how much stock is held, where it is stored, and how it is replenished. It plays a central role in balancing product availability with working capital efficiency.

5. Distribution & Logistics: The Complexity Multiplier

Distribution and logistics ensure that finished goods move efficiently from production facilities to end customers. This includes warehousing, transportation, order fulfilment, and coordination with retail and e-commerce channels. Modern distribution networks support multiple routes to market, including traditional retail, direct-to-consumer models, and omnichannel fulfilment.

Close coordination between manufacturers and retail partners supports effective replenishment, promotion execution, and service delivery.

Now that the full process is clearly defined, it becomes easier to examine where structural challenges are emerging across the consumer goods supply chain.

Key Challenges in the Consumer Goods Supply Chain

The challenges facing the industry are not temporary disruptions. They are systemic weaknesses that have accumulated over years of incremental decisions.

1. Fragmented Technology and Low Digital Maturity

Many consumer goods organizations operate with technology landscapes that were never designed to function as a unified system. Over time, new planning tools have been layered onto legacy ERP systems, while spreadsheets continue to fill visibility gaps. Different regions often rely on different platforms, resulting in fragmented and disconnected operations.

In stable environments, this fragmentation remained manageable through manual intervention. However, in volatile conditions, it creates significant blind spots. When disruptions occur, data must be consolidated across multiple systems, slowing response times and increasing the likelihood of errors.

2. Weak Data Governance and Limited Visibility

The effectiveness of digital systems depends on the quality and consistency of underlying data. Many organizations face challenges with inconsistent data definitions across functions and regions. Inventory records may not align with procurement data, supplier metrics may lack standardization, and forecasting inputs may vary significantly.

As a result, visibility becomes unreliable. Decision-makers may have access to dashboards but lack confidence in the accuracy of the information. In a supply chain environment where speed and precision are critical, unreliable data limits the ability to anticipate disruptions and identify emerging risks.

3. SKU Complexity and Operational Strain

Portfolio expansion has significantly increased operational complexity. The introduction of multiple product variations, formats, and packaging options has expanded the number of SKUs that organizations must manage.

Higher SKU volumes increase production changeovers, complicate forecasting, and add pressure on warehousing and distribution systems. Low-volume SKUs further distort demand patterns, reducing planning accuracy. Over time, this growing complexity places sustained pressure on operations and margins, often without immediate visibility into its full impact.

4. Deglobalization and Trade Volatility

Shifts in global trade dynamics have introduced greater uncertainty into sourcing strategies. Tariffs, geopolitical tensions, and regional trade realignments have altered cost structures and increased exposure to disruption.

Supply networks that are concentrated in specific regions are particularly vulnerable to sudden policy changes or supply interruptions. At the same time, managing cost pressures has become more difficult in an increasingly price-sensitive market. This creates ongoing tension between maintaining cost efficiency and managing exposure to external risks.

5. Retailer Power Shifts and Margin Pressure

Retailers are gaining greater influence through the expansion of private-label offerings and increased control over consumer data. At the same time, consumers are becoming more price-sensitive, placing additional pressure on branded products. This combination reduces pricing power for manufacturers and compresses margins. The balance of power within the value chain is shifting, increasing commercial pressure across the supply chain.

Having examined these challenges, the natural question arises: how is the industry responding?

The trends shaping 2026 are not abstract innovations. They are direct reactions to the structural pressures outlined above.

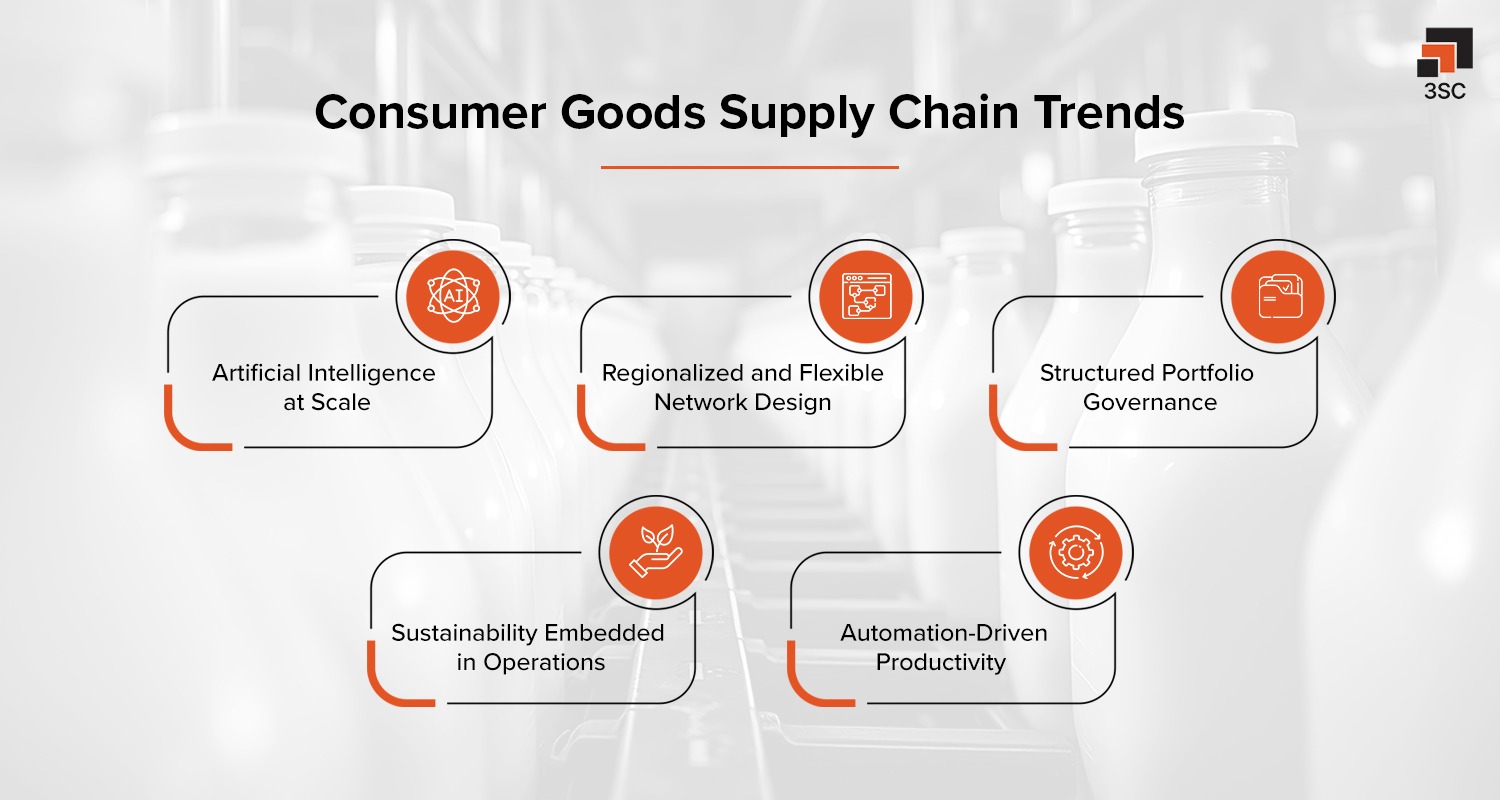

Consumer Goods Supply Chain Trends 2026: The Industry’s Response

Each of the following trends can be understood as both an evolution and a solution.

1. Artificial Intelligence at Scale

The use of AI across planning and execution systems is expanding rapidly. Organizations are applying AI to demand sensing, supplier risk modelling, production scheduling, and inventory optimization. These capabilities enable faster scenario analysis, improved demand signal interpretation, and earlier identification of potential disruptions. AI is becoming an integral part of how supply chain decisions are informed and executed.

2. Regionalized and Flexible Network Design

Companies are re-evaluating how sourcing and manufacturing networks are structured. There is a growing shift toward supplier diversification and the expansion of nearshore or regional production capabilities. The objective is to reduce dependency on single geographies and introduce greater flexibility into supply networks. These network structures are enabling faster adjustments to changes in trade policies, demand patterns, and transportation conditions.

3. Structured Portfolio Governance

Organizations are placing greater emphasis on structured portfolio management as SKU counts continue to expand. This includes the development of formal evaluation frameworks that assess product performance across dimensions such as profitability, cost-to-serve, operational impact, and strategic relevance. Portfolio decisions are becoming more data-driven and aligned with overall supply chain capabilities.

4. Sustainability Embedded in Operations

Sustainability is increasingly being integrated into core supply chain processes. Regulatory expectations and retailer requirements are driving the inclusion of ESG criteria in sourcing, packaging, and logistics decisions. Material selection, supplier evaluation, and transportation planning are being assessed with environmental considerations alongside traditional cost and service factors.

5. Automation-Driven Productivity

Automation is expanding across supply chain functions, particularly in planning, procurement, and manufacturing operations. Repetitive activities such as data reconciliation, reporting, and transactional coordination are increasingly being automated. This is accelerating process execution and reducing reliance on manual intervention across operational workflows.

With these industry shifts in motion, the next question is clear: how do they translate into sustained competitive advantage? Trends on their own do not create transformation. What determines success is how well those trends are integrated.

Best Practice: Turning Evolution into Advantage for Consumer Goods Supply Chain

Building a strong and resilient supply chain requires more than isolated improvements. It requires alignment across technology, data, sourcing, portfolio decisions, and organizational structure and this alignment must be maintained cohesively across the supply chain through:

- Ensuring consistent data flow across functions. Procurement, planning, manufacturing, and logistics operate from a shared source of truth, reducing reconciliation delays and improving decision accuracy.

- Strengthening scenario planning capabilities. Integrated systems enable teams to model demand shifts, sourcing disruptions, or cost changes quickly and respond with confidence.

- Actively managing portfolio complexity. SKU decisions are evaluated continuously to ensure growth remains aligned with operational capacity.

- Building adaptable supply networks. Diversified sourcing and flexible production footprints support smoother transitions when trade policies or market conditions shift.

- Aligning commercial and operational planning. Sales forecasts, promotional strategies, and production plans are coordinated to reduce friction and protect margins.

When the integration of functions reaches this level, the supply chain no longer reacts to challenges after they occur. It becomes proactive, coordinated, and strategically influential. What was once viewed primarily as a cost centre evolves into a growth engine, one that strengthens resilience, supports innovation, and enhances long-term competitive advantage. To truly strengthen resilience, businesses must actively implement these capabilities in a coordinated and sustained manner across the supply chain.

Conclusion: From Reactive Operations to Structural Advantage

The consumer goods supply chain is at a structural inflection point. The pressures defining 2026, from economic volatility and price-sensitive consumers to retailer leverage and geopolitical realignment, are not temporary challenges. They represent lasting structural shifts in how the industry operates.

Organizations that continue operating fragmented systems and reactive planning processes will struggle to keep pace. The profitability gap between mature and immature supply chains will widen further.

However, companies that integrate technology, strengthen data governance, redesign networks for resilience, formalize portfolio discipline, and embed sustainability into operations are building structural advantage. The future will not reward the most efficient supply chains built for yesterday’s stability. It will reward the most adaptable supply chains designed for tomorrow’s uncertainty.

And the organizations that recognize this shift and act decisively will define the next era of competitive leadership in the consumer goods industry.

Future-Proof Your CPG Supply Chain with 3SC

In a rapidly evolving CPG landscape, resilience, Integrated Business Planning (IBP), and real-time visibility are no longer optional. 3SC’s AI-powered supply chain and IBP solutions deliver predictive insights, scenario modelling, and end-to-end transparency - enabling CPG organizations to align demand, supply, and finance while anticipating risk and responding with confidence.

Connect with Team 3SC to build a smarter, AI-powered, and resilient CPG supply chain powered by integrated planning.

Related Read -

- Why Scaling Consumer Durable Supply Chains Depend on Strong IBP

- Turning Volatility into Strength: Why CPG Leaders Are Embracing Continuous Network Optimisation

- Top 4 Advantages of IBP for CPG Companies

- IBP Capabilities CPG Industries Must Look Out For

- Overcoming Challenges in the Adoption of IBP Solutions in the CPG Industry

- Digitalization of Integrated Business Planning: Transforming the CPG Industry

- How does IBP ace the financial and operational objectives of the CPG Industry?

- Integrated Business Planning: The Structural Backbone of Modern CPG Supply Chains

- Why the Next Advantage in CPG Supply Chains Isn’t Better Planning - It’s Better Decisions

- From Backbone to Growth Engine: How CPG Leaders Are Reimagining the Supply Chain