With more than a decade of experience working across supply chains, especially with automotive brands, I have seen one pattern become increasingly clear: automotive companies are not struggling because they lack logistics partners. They are struggling because the network has become too complex to manage through fragmented execution.

Across inbound parts management, plant logistics, finished vehicle movement, aftermarket distribution, and partner coordination, the same issue keeps showing up. When something goes wrong, the first question is usually, “Where is the shipment?” The second, often asked after multiple escalations, is, “Why did we not know sooner?”

That gap between execution happening and the right people knowing is where significant value quietly disappears from automotive supply chains. It leads to delayed decisions, premium freight, production risk, inventory buffers, service failures, and rising cost of detention and demurrage.

Closing this gap requires more than another logistics provider or another visibility dashboard. It requires a proper orchestration layer across the logistics network.

This is what the 4PL conversation in automotive should really be about. Not outsourcing more but coordinating better.

Why Automotive Supply Chains Are Different

Most industries deal with supply chain complexity. Automotive is in a different category.

A single Original Equipment Manufacturer (OEM) depends on thousands of direct and sub-tier suppliers across dozens of countries. Inbound parts move on precise schedules tied to production sequences. Outbound finished vehicles flow through yards, ports, rail networks, and dealer pipelines. Aftermarket channels run in parallel. Each of these flows has its own partners, systems, and performance metrics, and almost none of them talk to each other in real time.

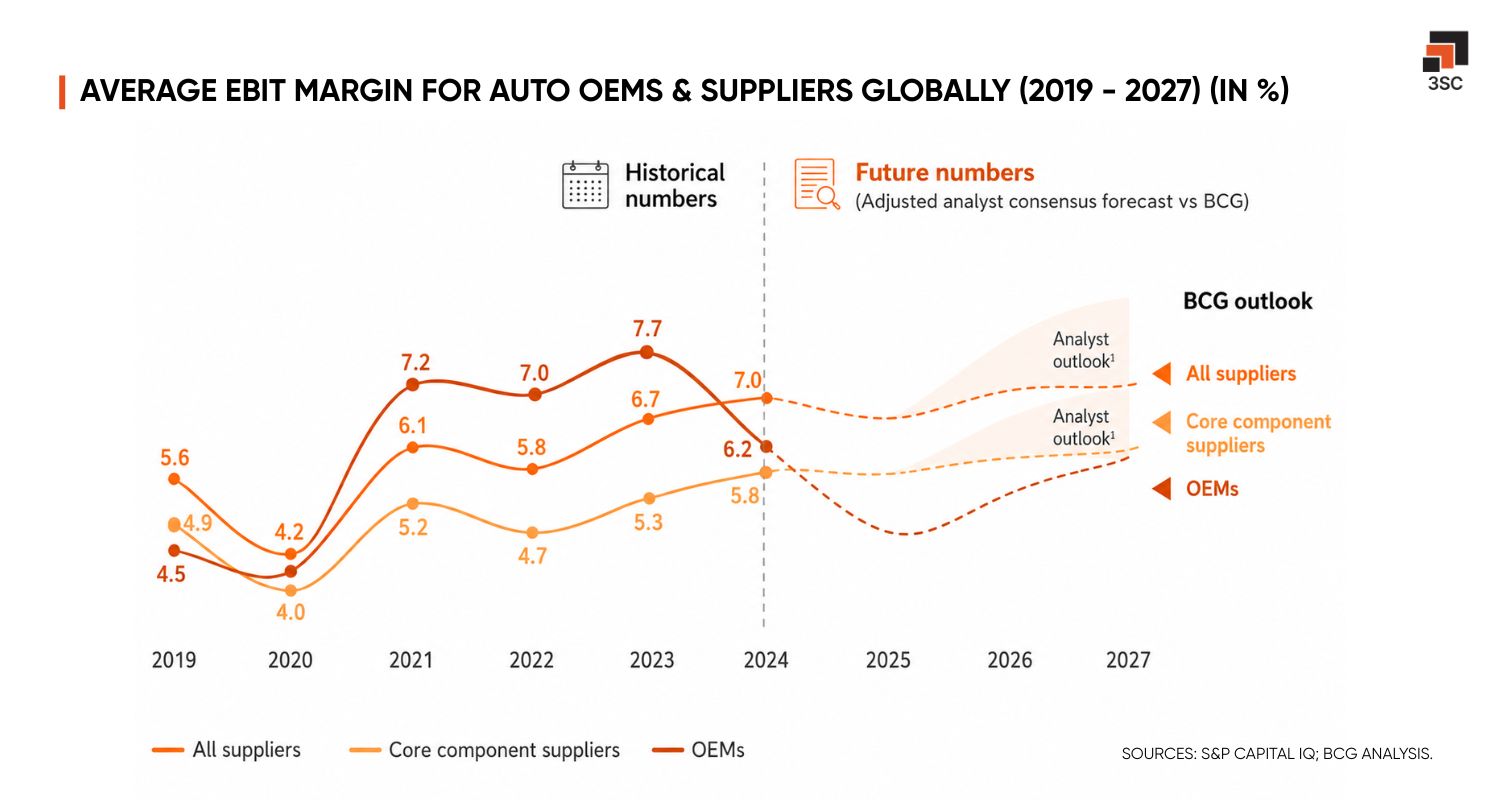

This fragmentation was already a systemic vulnerability. Now the industry is absorbing structural changes that make it significantly harder to manage. As per a recent research by BCG, Battery Electric Vehicle (BEV) program-level demand deviated from original forecasts by up to four times in the first half of 2025, both above and below plan, across China, Europe, and North America.

Electrification isn't just changing what's being built. It's introducing a new and much harder type of demand volatility into supply chains that were already running lean. The same study highlights that supply-chain fragility has surged as a concern among supplier executives, with investments in batteries and e-powertrain systems being capital-intensive, front-loaded, and difficult to redeploy when production plans shift.

In this environment, the classic just-in-time model, optimized for cost and efficiency, with thin buffers and high dependency on schedule adherence is increasingly fragile. But most automakers are unable to identify suppliers beyond tier one, meaning they don't know their lead times, production locations, or track records. When something disrupts a sub-tier supplier, the OEM often finds out last.

This isn't a technology problem. It's an operating model problem.

The Real Cost of Fragmented Execution

Today, most automotive companies already have multiple logistics partners. Inbound transporters, yard managers, port operators, customs brokers, freight forwarders, and last-mile distribution partners. The capability is there. The issue is that these partners operate in silos, each optimizing their own piece without a shared view of what's happening across the network.

The cost shows up in predictable places. Premium freight gets booked because a supplier's delay wasn't visible in time to reroute. Buffer inventory builds up because inbound visibility is poor. Carrier performance drifts because governance is inconsistent across regions. Exceptions get resolved through phone calls and spreadsheets rather than structured workflows.

None of these are catastrophic individually. But together, they create a steady drain on logistics cost and service performance. The issue is not just coordination failure, but limited visibility across stakeholders. When teams do not see the same risks, constraints, or updates in time, small gaps quietly turn into recurring inefficiencies.

Most companies have quietly stepped back from active supply chain risk management. Only about a quarter now discuss it at a senior level down from nearly half in 2023. The majority only pay attention when something breaks. In automotive, that's a dangerous way to operate.

What 4PL Actually Means in an Automotive Context

The term "4PL" gets used loosely. It's worth being precise about what it means and more importantly what it's supposed to do.

At its core, a 4PL manages the design, build, run, measurement and orchestration of all or part of an end-to-end logistics network, while delivering visibility, management control and optimization through an integrated technology platform. That's a more demanding mandate than it might initially sound.

The distinction from a 3PL is clear: a 4PL doesn't just execute a defined activity; it coordinates across multiple activities and parties to optimize network-wide outcomes. The difference is between doing and governing.

That shift is now being formally recognized. Gartner's inaugural 2025 Magic Quadrant for 4PL marks the category's evolution from visibility tools that tell you what's happening, to orchestration that determines what to do about it and owns the outcome.

For an automotive company, that difference plays out concretely. If a critical component is delayed at the port, visibility gives you a flag but, Orchestration gives you an assessment of production impact, remaining inventory cover at the plant, alternate routing options, expedited freight cost, and a recommended recovery action, coordinated across the carrier, the plant, and the supplier simultaneously.

That's not just a tracking upgrade. That's a fundamentally different operating model.

What a Stronger Orchestration Layer Actually Enables

I want to be specific about the value, because it's easy for this conversation to stay abstract.

A 4PL model doesn't deliver value through a single capability; it delivers it by connecting capabilities that currently operate in isolation. The four areas below represent where that connection creates the most meaningful difference in an automotive logistics context.

1. Exception management that actually protects production

The default in automotive logistics is reactive escalation; an exception becomes visible after service levels are affected, gets resolved manually, and is filed away. A proper orchestration model works differently. The moment early signals appear - delay codes, carrier ETAs, inventory thresholds; exceptions are routed through structured workflows, and the right response is triggered across all relevant parties before the production schedule is ever at risk.

2. Cost-to-serve that reflects trade-offs, not just spending

Logistics costs in automotive are rarely analyzed in context. Premium freight gets approved because it's faster. Detention accumulates because nobody is watching it. Load utilization is optimized by lanes rather than across the network. A 4PL model brings these together, so the business can see what a logistics decision actually costs relative to the service outcome it achieves, shifting the conversation from "how much did this shipment cost?" to "why did it cost what it did, and what would we do differently?"

3. Partner governance that scales

In a multi-plant, multi-region automotive network, maintaining consistent performance standards across dozens of logistics providers is one of the harder operational problems. Without a central governance layer, every plant manages its own vendor relationships; metrics are inconsistent, and accountability is difficult to enforce. A 4PL model standardizes KPIs, Service Level Agreement (SLA), escalation paths, and review cadences across the network, turning partner management into a repeatable capability rather than a series of individual relationships.

4. Decision support at the network level

The most valuable thing a 4PL can ultimately provide is the ability to evaluate options before committing to them. Can we absorb this delay without expediting? Which alternate carrier can cover this lane at short notice? What's the inventory impact if we hold this shipment? These are questions that require a connected view of logistics, inventory, production, and cost, and that's only possible when data from across the network flows into a single operating layer.

None of these capabilities are new in isolation. What changes with a proper orchestration model is that they stop being separate initiatives and start reinforcing each other. That's where the compounding value comes from and why the shift from execution to orchestration is structural, not incremental.

Why Now

The structural case for this model has been building for years. But several things have converged that make it genuinely urgent.

Electrification is restructuring supplier networks faster than most companies anticipated. New battery and e-powertrain suppliers are coming online with different geographic footprints, different lead times, and different risk profiles than the ICE suppliers they're replacing. Trade shifts and tariff uncertainty are forcing sourcing decisions that add complexity to logistics networks. And customer expectations like delivery precision, vehicle availability, and aftermarket service continue to rise.

At the same time, the technology infrastructure for orchestration is now mature enough to deliver on the promise. Real-time shipment visibility connected to TMS platforms, exception management workflows, and performance analytics are all available at scale. The barrier is no longer technology. It's the operating model and the organizational will to build the coordination layer around it.

Gartner's 2026 Logistics and External Manufacturing Outsourcing Trends Survey found that 42% of supply chain leaders already outsource to a 4PL, with a further 35% planning to do so within the next two years. That's not a niche movement. That's the beginning of a structural shift in how complex supply chains are managed.

The Decision That Actually Matters

The question for automotive supply chain leaders isn't whether to add another logistics partner or upgrade another TMS module.

It's whether to build a proper orchestration layer - one that connects suppliers, plants, carriers, yards, and distribution partners into a shared operating rhythm, and gives the business real-time visibility and decision support across that network.

That's a different kind of investment from traditional logistics outsourcing. It requires clarity on scope, strong data foundations, and a governance model that spans the network. It also requires accepting that the value isn't just in moving freight more efficiently; it's in making better decisions about how the whole system operates.

I've seen what automotive supply chains look like when that layer is missing. Capable people spending too much time on manual escalation. Cost that builds quietly and gets explained away. Disruptions that were visible in hindsight, but invisible at the time they mattered.

The companies that will run better automotive supply chains over the next decade aren't going to do it by signing better carrier contracts or hiring more planners. They'll do it by building the coordination capability that turns logistics execution into network intelligence.

That's the real value of 4PL in automotive. And it's overdue.