Key Takeaways

- Scope 3 emissions are often the largest and least visible part of a company’s carbon footprint.

- The biggest challenge is limited visibility across suppliers, logistics partners, customers, and product life cycles.

- Reporting remains inconsistent because companies use different methods, boundaries, and data assumptions.

- Companies must move gradually from broad estimates to supplier-specific, activity-based emissions data.

- Real Scope 3 progress happens when reporting informs sourcing, product design, logistics, and supply chain decisions.

Before a company can reduce its carbon footprint, it first has to answer a difficult question: where are its emissions really coming from?

For many businesses, the honest answer is uncomfortable. The majority of emissions are not inside their factories, offices, or company-owned vehicles. They are hidden across a sprawling value chain embedded in purchased materials, outsourced production, transport networks, packaging, customer use, and eventual disposal. And they are far larger than most companies publicly acknowledge.

According to a joint report by BCG and CDP, corporate supply chain emissions are, on average, 26 times greater than a company's combined Scope 1 and 2 emissions, yet only 15% of companies disclosing to CDP have set a Scope 3 reduction target.

That gap between scale and action is the central challenge of corporate climate strategy today.

What Are Scope 3 Emissions and Why Do They Matter So Much?

To understand the problem, it helps to understand the three-part structure of corporate emissions accounting.

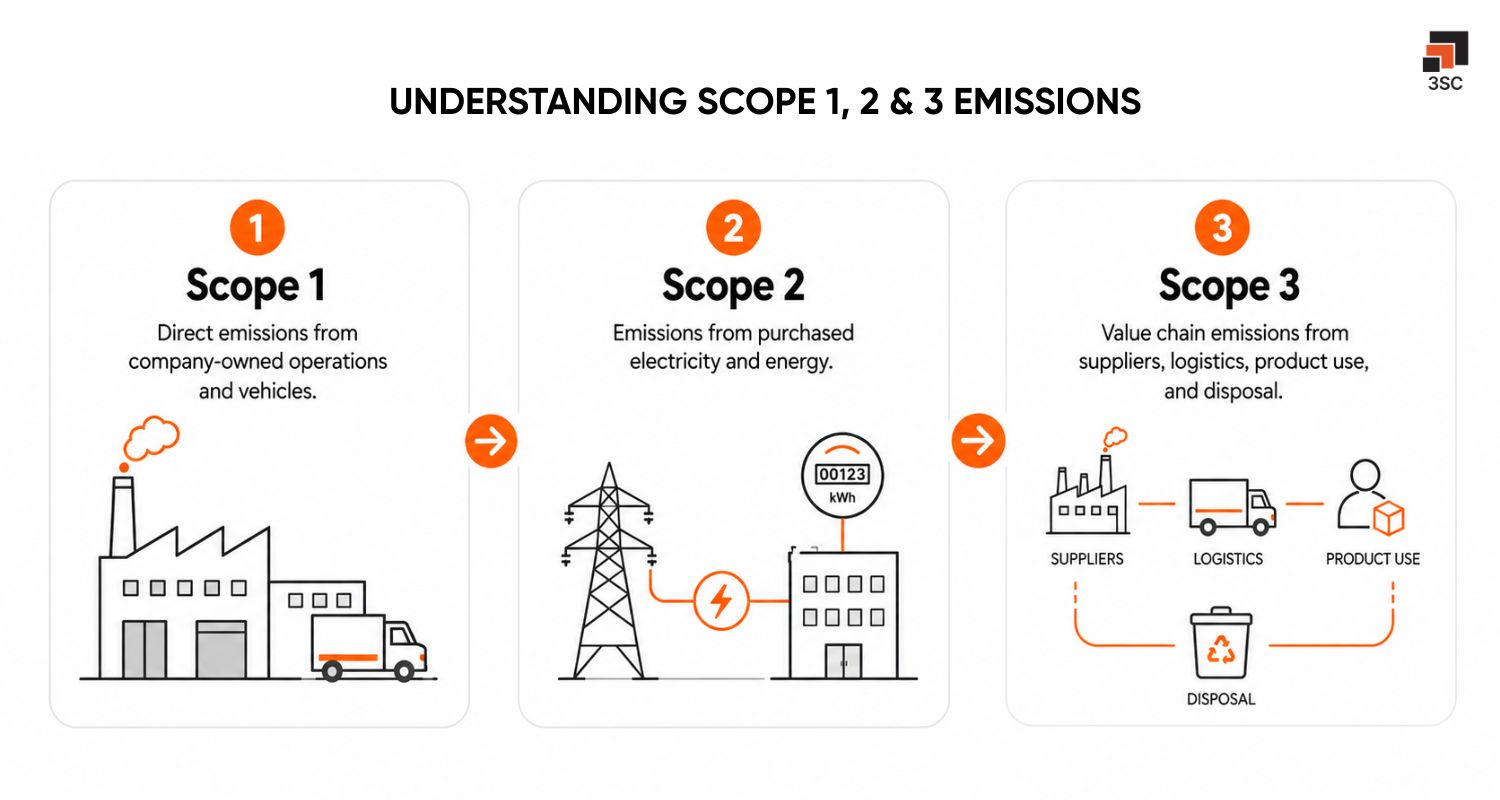

- Scope 1 covers direct emissions from sources a company owns or controls like its furnaces, vehicles, and production processes.

- Scope 2 covers purchased energy, primarily electricity. These two scopes are measurable, manageable, and increasingly well-reported.

- Scope 3 is everything else. It captures indirect emissions that occur across a company's entire value chain from the suppliers who grow, mine, and manufacture inputs, to the customers who use and eventually discard the finished product. The Greenhouse Gas Protocol divides Scope 3 into upstream categories (purchased goods, logistics, waste, business travel) and downstream categories (distribution, product use, end-of-life treatment).

For a company selling packaged food, electronics, pharmaceuticals, or industrial equipment, Scope 3 emissions surface at every stage: raw materials are extracted, components manufactured, goods shipped across continents, products used by customers, and packaging sent to landfill or recycling. None of these activities are controlled by the company. Yet all of them generate emissions on its behalf.

This is what makes Scope 3 both the most important and the most difficult dimension of corporate climate action.

The Measurement Problem: You Cannot Reduce What You Cannot See

Scope 3 emissions are difficult to measure because most companies lack reliable data from the full depth of their value chains.

A business typically knows its first-tier suppliers well. It may have contracts, audits, and established relationships with the companies that provide its packaging, raw materials, or logistics. But beyond that first layer, visibility fades quickly. A supplier depends on its own suppliers. Those suppliers rely on another network of producers, transporters, and subcontractors. Each layer adds complexity and distance.

The result is a simple but serious problem: you cannot accurately measure what you cannot map.

Companies also face genuine disagreement about where their Scope 3 responsibilities begin and end. Should the inventory include only major suppliers, or every tier? Should it cover customer usage, leased assets, employee commuting, investments? These boundary decisions vary widely from one company to another, making comparisons unreliable.

The challenge is compounded by the fact that supply chains are constantly shifting. Suppliers change, sourcing strategies evolve, and new logistics routes emerge. A carbon inventory that is accurate today may not reflect tomorrow's network.

As a result, most Scope 3 calculations rely on averages, estimates, and models rather than real supplier-level data. These approximations are a useful starting point, but they rarely provide an accurate picture of actual emissions. The measurement problem is not only technical. It is also a problem of visibility, trust, and coordination across a system that no single company fully controls.

Why Reporting is Still Inconsistent and Why That Creates Risk

Measurement alone would be manageable if companies at least reported consistently. But Scope 3 reporting remains highly uneven, and that inconsistency creates serious risks for investors, regulators, and the companies themselves.

A KPMG analysis found that while 73% of the world's largest companies now report on Scope 3 emissions, only 46% provide comprehensive disclosure of methodology, boundaries, and data quality, meaning more than half are reporting numbers without the context needed to evaluate them.

The root cause is methodological fragmentation. Some companies use a spend-based approach: multiplying the cost of goods and services by average emission factors. This is quick and useful when supplier data is unavailable, but imprecise because a higher purchase cost does not mean higher emissions, and a cheaper input is not always cleaner.

Other companies use life cycle assessment, activity-based calculations, or supplier-specific data. These are more accurate but require deeper engagement with partners who may lack the capacity, willingness, or systems to share that information.

Two companies in the same sector can therefore report Scope 3 emissions very differently, not because their actual footprints are different, but because they have drawn different boundaries, used different methods, and made different assumptions. One may include product use emissions; another may not. One may report all fifteen GHG Protocol categories; another may focus only on the easiest ones to calculate.

The danger is that these numbers can look precise without being meaningful. A company can appear to be making progress while the actual trajectory of its emissions stays hidden. Without common reporting standards and consistent methodology, Scope 3 disclosures risk becoming a compliance exercise rather than a genuine accountability mechanism.

Where Visibility Gaps Appear and Why They Are Hard to Close

Even companies that want to report accurately face structural gaps in their visibility. These gaps appear wherever a company depends on external partners for emissions data but lacks the access, influence, or tools to get it.

The most significant gap is beyond first-tier suppliers. Many companies engage their immediate suppliers on sustainability, but far fewer reach second or third-tier suppliers. This matters because some of the highest-emission activities like raw material extraction, energy-intensive manufacturing, agricultural production happens deep in the supply chain, far from direct view.

Downstream visibility is often even weaker. Companies tend to focus more attention on suppliers than on customers, because supplier relationships feel more manageable. But for products that consume energy during use (appliances, vehicles, electronics, industrial machinery), the downstream emissions can dwarf everything upstream. The emissions story continues long after the product is sold.

Logistics creates another persistent blind spot. Freight emissions may be spread across multiple carriers, transport modes, warehouses, and subcontractors. A company may know that a shipment moved from one region to another without knowing the fuel type, vehicle load, or route-level emissions behind that movement.

Small and medium-sized suppliers create a different kind of gap: a capability gap. Many lack the tools, budgets, or technical knowledge to calculate and share emissions data. When large companies ask them for carbon information, the response may be incomplete, delayed, or based on rough estimates, not because of unwillingness, but because the infrastructure to do better simply does not exist.

Closing these gaps requires more than data requests. It requires investment in supplier capacity, shared tools, and long-term collaboration.

How Can Companies Close Scope 3 Visibility and Reporting Gaps?

Scope 3 progress is not about achieving perfect data before taking action. It is about building the right habits, systems, and relationships and improving incrementally over time.

1. Map before you measure

Start with a value chain map, not a spreadsheet. Identify where emissions are likely concentrated, which supplier categories carry the most weight, and where data is simply missing. Prioritisation matters and no company can solve every Scope 3 category at once, and trying to do so leads to shallow coverage everywhere rather than meaningful progress anywhere.

2. Move from estimates to evidence, gradually

Spend-based estimates are a legitimate starting point, not an end state. The goal is to progressively replace industry averages with activity-based and supplier-specific data, category by category, tier by tier. Digital platforms, supplier portals, and automated data-sharing tools make this more achievable than it was even three years ago.

3. Treat suppliers as partners, not data sources

Suppliers (especially smaller ones) will not improve reporting or performance if they only receive requests and deadlines. The companies making the most progress offer training, shared tools, phased timelines, and technical assistance alongside their expectations. Engagement that feels like a partnership produces better data and better outcomes than engagement that feels like an audit.

4. Be honest about what you do not know

A credible Scope 3 report should explain not just the number, but how reliable it is, which categories are included, which are excluded, what methods were used, and where gaps remain. Transparency about limitations builds more trust than polished figures with weak foundations, and it protects companies from the greenwashing risk that incomplete reporting creates.

5. Connect reporting to decisions

Scope 3 data only has value if it changes something. That means using emissions insights to inform supplier selection, product design, logistics choices, and capital allocation, not just annual disclosures. When reporting connects to decisions, it becomes a management tool rather than a compliance exercise.

6. Redesign, don’t just account

The deepest reductions come from changing how products are built, moved, used, and recovered, not from more accurate accounting of the same processes. Circular packaging, cleaner logistics, recycled materials, product life extension, and take-back programmes reduce emissions at the source. That is where the real leverage is.

Closing Scope 3 gaps is not a one-time reporting project; it is a continuous shift from limited visibility to better decisions, stronger partnerships, and lower-emission supply chains.

The Road Ahead

Scope 3 emissions are no longer a niche sustainability concern. Regulators like the EU's Corporate Sustainability Reporting Directive now requires disclosure of material Scope 3 emissions, and similar requirements are advancing in other markets.

Investors have also started paying attention: a PwC survey found that 76% of investors consider a company's climate strategy in their investment decisions, with particular focus on how comprehensively it addresses Scope 3.

Customers and business partners are increasingly requesting carbon data from suppliers, making visibility a commercial requirement as well as a reporting one.

At the same time, the tools are improving. Digital traceability systems, machine learning-based anomaly detection, and collaborative data-sharing platforms are making it increasingly feasible to move from approximation toward real-time emissions visibility.

But the fundamentally human elements remain just as important as the technical ones. Progress on Scope 3 depends on trust between companies and their supplier networks. It depends on whether smaller partners receive support rather than only pressure. It depends on whether companies are willing to look past the numbers and rethink how their products are designed, moved, used, and recovered.

The organisations that lead will not be the ones with perfect data from day one. They will be the ones honest enough to identify their gaps, disciplined enough to close them, and bold enough to act before every number is certain.

Scope 3 emissions are the hardest part of supply chain sustainability. They are also where the greatest leverage lies, because once a company learns to see beyond its own walls, it can begin reducing emissions across the entire system that brings its products to life.